Getting hurt on the job can turn your world upside down in an instant. In Ontario, worker’s compensation benefits are there to act as a critical safety net. This system, managed by the Workplace Safety and Insurance Board (WSIB), is designed to provide financial support and cover your medical care when you’re injured at work, taking the immediate burden of lost paycheques and treatment costs off your shoulders.

Quick answer: Workplace injury compensation in Ontario usually means a WSIB claim, not a lawsuit against your employer. Depending on the facts, WSIB may cover loss-of-earnings benefits, health care, return-to-work support, permanent impairment awards, and survivor benefits. The safest first steps are to report the injury, get medical attention, file the right forms on time, and get advice quickly if WSIB denies the claim, reduces benefits, or pushes an unsafe return-to-work plan.

Understanding Your Rights After a Workplace Injury

When an accident happens at work, the first and most important step is knowing your rights. The WSIB system is built on a “no-fault” principle. This is key—it means you don’t have to prove your employer was careless or did something wrong to get benefits. The only thing that matters is that your injury happened while you were doing your job.

This guide will break down the entire process for you, step by step. We want to show you how the system is set up to support workers across Ontario, from the GTA to the smallest towns. There’s a structured path forward to help you recover with confidence.

What Is the Purpose of WSIB?

Think of the WSIB as a massive, provincially required insurance plan that nearly every employer in Ontario pays into. It’s there to protect both sides. For you, the worker, it’s a lifeline when you need it most. For employers, it offers protection from being sued directly by an injured employee, which helps create a more predictable and stable business environment for everyone.

At its heart, the WSIB system is a trade-off. Workers give up the right to sue their employer for a workplace injury in exchange for guaranteed, no-fault benefits to support their recovery and return to work.

Your Journey Through the System

Navigating the WSIB can feel like a maze at first, but once you understand the key stages, it becomes much easier to handle. The following sections will walk you through everything you need to know, from checking if you’re eligible and filing your first report to appealing a decision if things don’t go your way.

Our goal here is to give you a clear roadmap, helping you secure the worker’s compensation benefits you’re entitled to under Ontario law. While this guide focuses specifically on the WSIB system, you can also learn more about the broader fundamentals of the law on personal injury in Ontario. It can also be helpful to understand the kinds of medical evaluations involved, such as an occupational health assessment, which you may encounter during your claim.

The Types of WSIB Benefits Available to You

Getting hurt on the job isn’t just a physical setback; the financial stress can hit just as hard. In Ontario, workers’ compensation is designed to be a full-circle support system, helping you tackle the different challenges that pop up while you’re recovering.

It helps to think of these benefits not as a single cheque, but as a complete toolkit provided by the Workplace Safety and Insurance Board (WSIB). Each tool has a specific job, whether it’s covering your lost wages, paying for medical treatments, or helping you adapt to long-term changes. Knowing what’s in the toolkit means you know what you’re entitled to.

Let’s break down the core benefits so you can see which ones fit your situation and focus on what truly matters: getting better.

1. Replacing Your Lost Income

For most people, the first question that comes to mind is, “How will I pay my bills without a paycheque?” This is exactly what Loss of Earnings (LOE) benefits are for. They are the backbone of WSIB support, designed to replace a large chunk of your income when you can’t work.

LOE benefits cover 85% of your net average earnings—that’s your take-home pay after taxes and deductions, right before the injury happened. So, if you typically brought home $1,000 a week, your LOE benefit would be about $850 per week. These payments are meant to continue until you can safely get back to your job, or until you turn 65.

2. Covering Your Medical and Recovery Costs

Beyond your wages, the WSIB also provides extensive Health Care Benefits so you can get the medical care you need without having to pay out of your own pocket. This coverage is incredibly broad, paying for a whole range of treatments and services that are essential for your recovery.

Here’s a quick look at what’s typically covered:

- Medical Treatments: Visits to your family doctor, specialists, and any required hospital services.

- Prescription Medications: The prescriptions you need to manage pain or treat your specific condition.

- Therapy and Rehabilitation: Services like physiotherapy, chiropractic adjustments, and occupational therapy to help you regain function.

- Medical Devices and Equipment: This could be anything from crutches or a back brace to major modifications to your home if your injury is severe.

The whole point is to remove money as a roadblock to your recovery. The WSIB pays approved healthcare providers directly, so you shouldn’t have to worry about fronting the cash for your authorized treatments.

3. Compensation for Permanent Injuries

Unfortunately, some workplace injuries leave behind a permanent impairment—a physical or psychological condition that won’t ever fully heal, even after you’ve made the best possible recovery. If this happens to you, you might be eligible for a Non-Economic Loss (NEL) award.

A NEL award is a one-time, lump-sum payment. It’s meant to acknowledge the permanent impact the injury has had on your life outside of work, compensating you for things like the loss of enjoyment of life or ongoing physical pain.

The size of the NEL award is decided by a doctor who assesses the degree of your permanent impairment based on a specific rating guide. For example, a factory worker in Burlington who loses partial use of their hand in a machinery accident would receive a NEL award calculated on how severe that permanent loss of function is.

4. Support for Families After a Tragedy

In the most heartbreaking cases where a worker dies from a workplace injury or illness, the WSIB provides Survivor’s Benefits. This support is there to provide a financial lifeline to the person’s spouse, dependent children, and other dependants.

Survivor’s benefits typically include:

- A lump-sum payment made directly to the surviving spouse.

- Ongoing monthly payments for the spouse and any dependent children.

- Access to bereavement counselling to help the family cope.

- Assistance with funeral and transportation costs.

This support is absolutely vital. It helps ensure that a family isn’t thrown into a financial crisis during an unimaginably difficult time, offering them a small measure of security when they need it most.

To help you see it all at a glance, here’s a quick summary of the main benefits the WSIB provides.

WSIB Benefits Explained

| Benefit Type | What It Covers | Common Example |

|---|---|---|

| Loss of Earnings (LOE) | Replaces 85% of your net take-home pay while you are unable to work. | A construction worker who can’t work due to a back injury receives weekly payments. |

| Health Care Benefits | Pays for medical treatments, prescriptions, therapy, and necessary equipment. | A chef who burns their hand gets their specialist visits and medication costs covered. |

| Non-Economic Loss (NEL) | A one-time payment for a permanent physical or psychological impairment. | An office worker develops chronic pain after a fall and receives a lump sum. |

| Survivor’s Benefits | Financial support for dependants if a worker dies from a work-related cause. | A spouse receives a lump sum and monthly payments after their partner’s fatal accident. |

Understanding these categories is the first step in navigating the WSIB system and making sure you get the full support you’re entitled to.

Workplace Injury Compensation in Ontario: What to Check in 2026

If you searched for workplace injury compensation Ontario, you are probably trying to answer two questions at once: what can WSIB pay, and what should you do if the amount or decision seems wrong? A strong claim usually comes down to matching the right benefit category with the right proof.

Key items to review early include:

- Loss-of-earnings benefits: The Office of the Worker Adviser explains that full LOE benefits are generally calculated at 85% of net average earnings. WSIB uses net average earnings to decide the payment amount, so wage records, overtime history, and pre-injury work patterns can matter.

- Health care and rehabilitation: Keep receipts, referrals, treatment notes, and restrictions. Coverage disputes often turn on whether treatment is reasonable, necessary, and connected to the workplace injury.

- Return-to-work pressure: A modified-duty offer should respect your medical restrictions. If the proposed job is unsafe or does not match your functional abilities, put your concerns in writing rather than simply refusing.

- Appeal deadlines: Many WSIB decisions require a formal objection within a strict timeline. A denial letter, benefit reduction, return-to-work decision, or NEL award decision should be reviewed promptly.

- 2026 benefit context: WSIB announced a 2.0% cost-of-living adjustment for benefit recipients beginning January 1, 2026. That does not mean every disputed claim is automatically recalculated in your favour, but it is a reminder to check current figures, earnings records, and benefit calculations carefully.

For official background, review WSIB’s loss-of-earnings benefit information, the Office of the Worker Adviser’s LOE benefit guide, and WSIB’s 2026 annual indexing letter. If the math, medical restrictions, or appeal route is unclear, getting legal advice before the deadline can prevent avoidable mistakes.

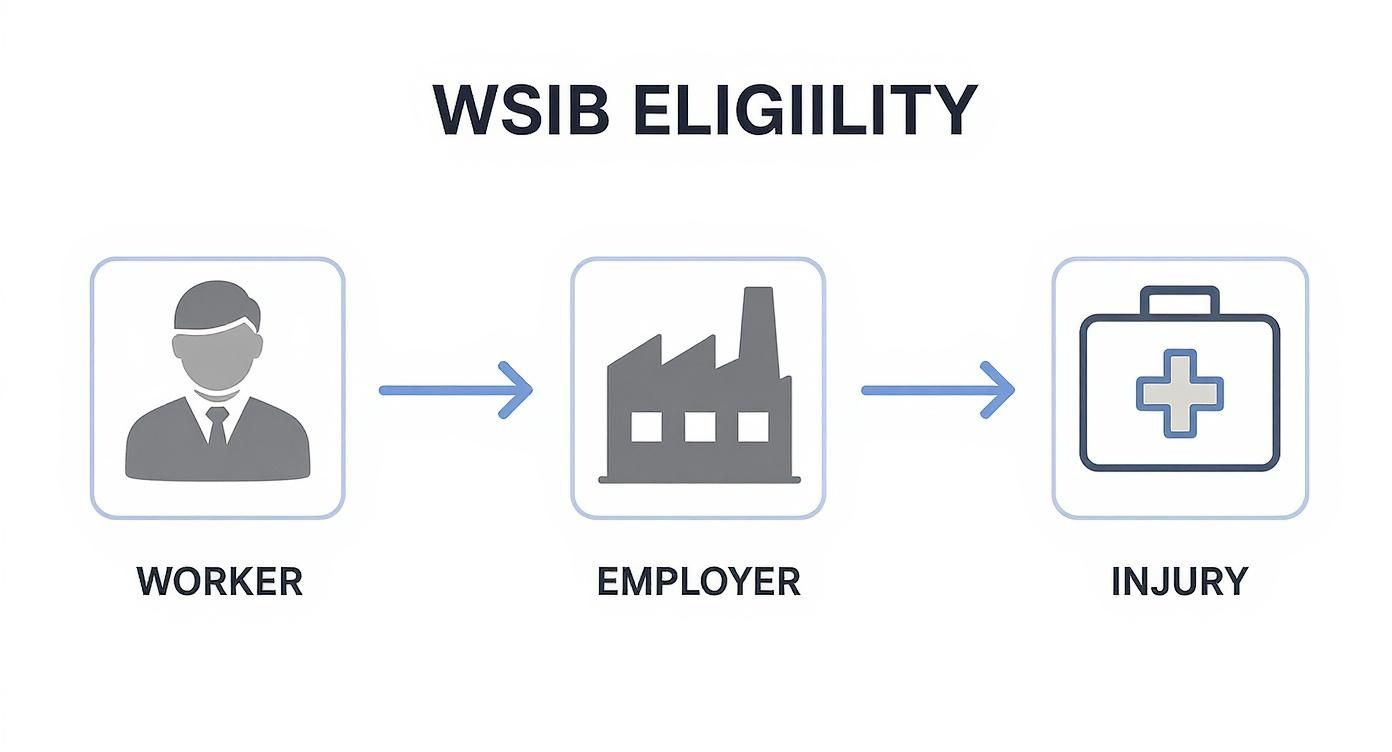

How Do I Know if I Qualify for WSIB?

Getting hurt at your workplace doesn’t automatically mean you’re covered by workers’ compensation. In Ontario, the Workplace Safety and Insurance Board (WSIB) has a specific set of rules, and understanding them is the first real step in getting the benefits you might be entitled to.

Think of it like a three-legged stool. For your claim to stand, all three legs need to be solid. If one is shaky or missing, the whole thing can fall apart.

So, what are these three legs? A successful WSIB claim hinges on proving these three things:

- You are legally considered a ‘worker’.

- Your employer is a ‘covered employer’ who pays into the WSIB system.

- Your injury or illness happened ‘out of and in the course of employment’.

Let’s dig into what each of these really means.

The Three Pillars of WSIB Eligibility

First, the WSIB has a specific definition of a ‘worker’. This covers most people you’d expect—full-time, part-time, temporary, and even seasonal employees. Where it gets tricky is with independent contractors, consultants, or some high-level executives, who often aren’t automatically covered. This is a common stumbling block for many people.

Second, your employer must be a ‘covered employer’. The vast majority of businesses in Ontario are legally required to have WSIB coverage, especially in industries like construction, manufacturing, and retail. They pay premiums that fund the whole system. However, some sectors like banking or telecommunications might be exempt, although they can choose to opt-in voluntarily.

Finally—and this is usually the most debated part—your injury has to be directly tied to your job. This is the official “arising out of and in the course of employment” test. It boils down to one simple question: were you doing something for your employer’s benefit when you got hurt?

At its core, the WSIB is asking: Was the activity that caused your injury directly linked to your job duties? If you can confidently say yes, you’re on the right track.

Real-World Scenarios from the GTA

To make this less abstract, let’s look at a couple of everyday examples you might see across the Greater Toronto Area.

-

The Obvious Case: A warehouse worker in Brampton feels a sharp pain in their back while lifting a heavy box. This is a textbook work-related injury. The action (lifting) was a core part of their job, making the WSIB claim straightforward.

-

The Gradual Injury: An office administrator in downtown Toronto develops severe carpal tunnel syndrome after years of constant typing. This isn’t a single event, but a repetitive strain injury that developed over time because of their work. It’s absolutely covered.

Navigating the Grey Areas

Of course, not every situation is so black and white. What happens when you’re not physically at your workplace or on the clock in the traditional sense? This is where WSIB has to take a much closer look.

Here are a few common grey areas:

- Work-Related Travel: A sales rep from Mississauga is in a car accident while driving to a client’s office. Since that travel was an essential part of their job, their injuries would almost certainly be covered by WSIB.

- Company Events: An employee from Burlington slips on a wet floor at the annual company holiday party. If the employer encouraged or expected staff to be there, it’s often considered a work function, and an injury would likely be deemed work-related.

Figuring out where you stand is crucial. WSIB is a specific system for work-related injuries, and it’s quite different from other benefits. For injuries that happen outside of work, you’ll need to look at other options. Our guide on accident benefits in Ontario is a great resource for that.

By taking a hard look at your situation and measuring it against these three pillars, you’ll have a much clearer idea of whether you qualify for WSIB coverage.

Filing Your WSIB Claim Step by Step

The moments after a workplace injury are often confusing and stressful. Your first priority is, of course, your health. But knowing the right steps to file a claim with Ontario’s Workplace Safety and Insurance Board (WSIB) is just as critical for protecting your right to worker’s compensation benefits.

The good news is that the process is manageable when you break it down. It’s a coordinated effort between you, your employer, and your doctor, and it all runs on some very strict deadlines. Let’s walk through it together, from the moment the injury happens to getting all your paperwork in order.

This flowchart shows how the key players connect after a workplace injury.

As you can see, it all starts with you and your injury, which then brings your employer into the picture through a mandated reporting process.

What to Do Immediately After an Injury

There are two things you absolutely must do right after getting hurt at work. These actions lay the groundwork for your entire claim.

-

Get Medical Help Right Away: Your health comes first. Get first aid on-site immediately. If the injury is more serious, head to the nearest clinic or emergency room. Make sure you tell the healthcare provider that your injury happened at work—this is a crucial detail for their records and reporting.

-

Tell Your Employer About the Injury: You need to let your supervisor, manager, or another person in charge know what happened as soon as possible. It’s always a good idea to follow up in writing, even with a simple email or text, to create a clear record of when you reported it.

If you wait too long to report your injury, it can cause problems down the road. The WSIB might start asking why there was a delay.

The Three Big Reporting Deadlines

When it comes to the WSIB claims process, the clock is always ticking. Three different reports have to be filed, and each one has its own non-negotiable deadline. Missing them can put your benefits at risk.

-

You (The Worker): You have six months from the date you were injured (or from when you learned you have an occupational disease) to file your claim with the WSIB. Six months sounds like a long time, but you should file as soon as you possibly can.

-

Your Employer: Once your employer learns about the injury, they have just three business days to report it to the WSIB. They do this by submitting a Form 7 (Employer’s Report of Injury/Disease).

-

Your Doctor: Your treating physician must send a Form 8 (Health Professional’s Report) to the WSIB within 72 hours of seeing you for your work-related injury.

These tight timelines are there for a reason. They ensure all the important information is gathered while it’s still fresh, which helps the WSIB make a fair and timely decision on your claim.

Filling Out Your Form 6 Report

The most important piece of paper you’ll handle is the Form 6 – Worker’s Report of Injury/Disease. This is your side of the story, your official account of what happened, and it’s the foundation of your claim for worker’s compensation benefits. You can fill it out online on the WSIB’s website, over the phone, or by mailing in a paper copy.

When you’re completing your Form 6, be as precise and detailed as you can. You’ll need to provide:

- Your personal info (name, address, SIN)

- Your employer’s details

- A step-by-step description of the incident (what, where, and when)

- A clear explanation of your injuries

- Information about the medical care you’ve received

Just be honest and stick to the facts. Exaggerating your injuries or giving misleading information can get your claim denied and could even lead to serious penalties.

Your WSIB Claim Documentation Checklist

Putting together a strong claim is all about being organized. Gathering the right documents and information from the start will make the entire process smoother and help you avoid frustrating delays.

Before you get started, it’s a good idea to gather all your documents in one place. This checklist will help you build a complete and compelling file for your claim.

| Document or Information | Why It’s Essential | How to Obtain It |

|---|---|---|

| Your WSIB Claim Number | You’ll need this number for every single communication with the WSIB. | The WSIB will assign this to you once your claim is officially registered. |

| Medical Records | These reports, notes, and test results are the objective proof of your injury. | Request copies from your family doctor, any specialists, therapists, or hospitals you’ve visited. |

| Proof of Earnings | This shows the WSIB how much you were making so they can accurately calculate your wage-loss benefits. | Gather your pay stubs from the four weeks immediately before your injury. |

| Witness Information | If someone saw what happened, their account can help support your version of events. | Get the names and contact information of any coworkers who witnessed the incident. |

| A Personal Log or Journal | A simple notebook is perfect for keeping track of appointments, conversations, and key dates. | Keep a running log of doctor’s visits, names of WSIB staff you speak with, and notes from phone calls. |

Having these items ready will show that you’re organized and serious about your claim.

Once your claim is filed, the WSIB will assign a case manager to it. They will review everything—your Form 6, your employer’s Form 7, and your doctor’s Form 8—to decide if you’re eligible for benefits. Being proactive and keeping everything in order is your best strategy for a smooth process.

What to Do If Your WSIB Claim Is Denied

Getting a letter from the Workplace Safety and Insurance Board (WSIB) saying your claim has been denied can feel like a punch to the gut. You’re already dealing with an injury, and now this? It’s completely normal to feel overwhelmed, angry, and uncertain about what comes next.

But here’s the most important thing to remember: a denial is not the end of the road. It’s simply the start of the appeals process.

You have a right to fight the WSIB’s decision. In fact, many claims that are initially rejected get approved on appeal. The trick is to understand exactly why they said “no” and then build a stronger case. This is your chance to clear up any confusion, submit new information, and fight for the worker’s compensation benefits you need.

Why Do WSIB Claims Get Denied?

Before you can fight back, you need to know what you’re up against. The WSIB’s decision letter is your starting point—it should explain their reasoning. While every situation is different, most denials boil down to a handful of common problems.

Figuring out the “why” is everything, as it tells you exactly what you need to fix in your appeal.

Here are some of the most frequent reasons for a denial:

- Not Enough Medical Proof: Sometimes, the doctor’s notes aren’t detailed enough. The WSIB might not be convinced your injury is serious or that it was directly caused by your work activities.

- A “He Said, She Said” Situation: Your employer might claim your injury happened outside of work. Or, the WSIB might decide a pre-existing condition is the real culprit, not your job.

- You Missed a Deadline: The WSIB has very strict timelines for reporting an injury and filing a claim. If you miss them, it can lead to an automatic rejection.

- The WSIB Thinks You’re Not Cooperating: If they feel you aren’t following your doctor’s orders, skipping treatment, or missing mandatory medical exams, they can stop your benefits.

Your Roadmap to a WSIB Appeal

The WSIB has a formal, step-by-step system for appeals. You don’t just call up your original case manager and ask them to change their mind. You have to escalate it up the ladder.

The appeals process is your legally protected path to a second opinion. It ensures that another, more senior decision-maker reviews your file with a fresh set of eyes.

Think of it as a multi-stage process where you have to clear each level before moving to the next.

Step 1: File the Intent to Object Form

This is your first move. You need to fill out and send in an Intent to Object form. Pay close attention to the deadline: you have six months from the date on the decision letter to get this form to the WSIB. This simple document officially registers your disagreement and keeps your right to appeal alive.

Step 2: The Appeal Goes to an Appeals Resolution Officer (ARO)

After you file the form, your case gets handed over to an Appeals Resolution Officer, or ARO. This person works independently and wasn’t involved in the first decision. They will review everything—your file, your employer’s reports, all the medical documents—and might call you to get more information.

The ARO might try to settle things through mediation. If that doesn’t resolve it, they will issue a new formal decision in writing. Be prepared to wait, as this part of the process can take a few months.

Step 3: Appeal to the Workplace Safety and Insurance Appeals Tribunal (WSIAT)

If the ARO doesn’t rule in your favour, you have one final option: the Workplace Safety and Insurance Appeals Tribunal (WSIAT). This is a big deal. The WSIAT is a completely separate and independent body from the WSIB, acting as the final say on workplace insurance disputes in Ontario.

An appeal to the WSIAT is more like a formal hearing. You or your lawyer will present your case, submit evidence, and make legal arguments. The WSIAT’s decision is final and binding.

It’s also important to know that WSIB isn’t the only safety net. If your injury keeps you off work for a long time, you should look into all your options. For example, exploring long-term disability insurance might provide another source of financial support while you recover.

When You Should Contact a Lawyer for Your WSIB Claim

While you can handle a straightforward WSIB claim on your own, the system can get complicated, fast. The key is knowing when to spot the warning signs that your claim is heading for trouble. Deciding to call a lawyer might be the most important move you make to protect your right to worker’s compensation benefits.

Think of a lawyer as a seasoned guide who knows the WSIB system inside and out. They understand the policies, the deadlines, and exactly what kind of evidence is needed to build a convincing case. Getting advice early on can help you avoid simple mistakes that could sink your claim and ensure you get the full support you’re entitled to under Ontario law.

Red Flags That Signal You Need Legal Advice

Some situations are immediate red flags, telling you it’s time to get professional legal help. If any of the following happens, it’s a clear sign your claim could be in jeopardy and you need an advocate in your corner.

-

Your Employer Disputes Your Claim: Is your employer saying the injury didn’t happen at work? Are they questioning how serious it is, or even trying to talk you out of filing a claim? This is a major problem. A lawyer can shield you from that pressure and make sure your version of events is properly recorded.

-

The WSIB Denies Your Claim: A denial letter is the most obvious sign you need help. A lawyer will dig into the WSIB’s reasoning, find the weak spots in their decision, and get a formal appeal started for you.

-

Your Benefits Are Reduced or Cut Off: If your benefit payments suddenly stop or get slashed, a lawyer can find out why. If the decision was unfair or wasn’t backed by proper medical evidence, they can challenge it.

-

You Have a Permanent Impairment: Figuring out a Non-Economic Loss (NEL) award for a permanent injury is incredibly complex. A lawyer’s job is to ensure the impairment rating truly reflects your condition, which helps maximize the compensation you receive for the long-term impact on your life.

When your claim involves a serious or permanent injury, the financial stakes are incredibly high. A lawyer acts exclusively as your advocate, ensuring your medical evidence is compelling and your case is presented in the strongest possible light during the appeals process.

The Strategic Advantage of Legal Representation

A lawyer does much more than just fill out forms. They take over all the communication with the WSIB, gather the necessary medical reports, and represent you in hearings, whether it’s with an Appeals Resolution Officer or at the Workplace Safety and Insurance Appeals Tribunal (WSIAT). If your WSIB claim is denied, you may need to gather further medical and legal support, and a specialized medico-legal consultancy could provide crucial expert opinions to strengthen your appeal.

At the end of the day, hiring a lawyer levels the playing field. The WSIB and your employer have experts on their side; you deserve to have one on yours, too. These situations often overlap with other workplace issues, and understanding your full rights under Ontario’s employment law can give you a much clearer picture. An expert makes sure every angle of your case is handled correctly from beginning to end.

Common Questions About Worker’s Compensation in Ontario

When you’re dealing with a workplace injury, a million questions can race through your mind. The WSIB system, while helpful, can feel complicated. Let’s clear up some of the most common questions we hear from injured workers across Ontario, from our neighbours in Burlington to clients throughout the GTA.

Can I See My Own Doctor for a WSIB Claim?

Absolutely. You have the right to choose your own doctor or other healthcare providers. The key is to tell them right away that your injury happened at work. This ensures they fill out the proper WSIB forms correctly and get them submitted on time.

Keep in mind, though, that the WSIB might also ask you to see a specialist they’ve selected for an independent medical assessment. This is a normal step in their process to get a complete picture of your injury and how it affects you.

How Long Do WSIB Wage Loss Benefits Last?

This is a big one. Loss of Earnings (LOE) benefits aren’t a permanent solution; they’re designed to support you while you recover. These payments will typically continue until one of three things happens:

- You’ve medically recovered from your workplace injury.

- You’re able to go back to work and earn what you were making before you got hurt.

- You turn 65 years old.

There’s a specific rule for those injured closer to retirement age. If you were 63 or older when the injury occurred and you’re still impaired at age 65, your benefits could be extended for up to two more years.

For anyone facing a long-term or permanent disability, it’s also smart to look at other potential supports. Learning how to apply for CPP disability benefits can open up another critical source of financial stability.

It is against the law for your employer to try and stop you from reporting an injury or to punish you for filing a WSIB claim. This is called ‘claim suppression,’ and it’s illegal in Ontario.

If you ever feel pressured by your employer not to file a claim, or if your job is threatened, you need to report it to the WSIB immediately. This is also a situation where getting legal advice is crucial to protect yourself.

Navigating a WSIB claim can be challenging, but you don’t have to do it alone. At UL Lawyers, our experienced team is dedicated to helping injured workers across Ontario secure the benefits they deserve. If your claim has been denied or you’re facing difficulties, contact us for a free, no-obligation consultation today at https://ullaw.ca.

Additional Considerations From Related Guides

The following points consolidate useful material from closely related UL Lawyers resources that covered overlapping search intent. They are included here so readers can find the strongest version of the guidance in one place.

From: Understanding the Benefits of Workers Compensation in Ontario

The Core WSIB Benefits That Support Your Recovery

When you’re hurt on the job, your main focus should be on getting better. But it’s hard to do that when you’re worried about medical bills and lost income. That’s exactly why the WSIB system exists.

Think of it as a safety net designed to catch you. It provides a whole suite of benefits to cover everything from your paycheque to your prescriptions. Let’s walk through what you’re entitled to, breaking down the jargon so you know exactly what support is available.

Loss of Earnings (LOE) Benefits

The first question on everyone’s mind is, “How will I pay my bills?” This is where Loss of Earnings (LOE) benefits step in. They are the most immediate and critical form of support, replacing the income you’ve lost because you can’t work.

If your claim is approved, the WSIB pays you 85% of your net average earnings—that’s your take-home pay before you got hurt. They calculate this based on your regular wages, overtime, and any other income to get a fair number. These payments keep coming as long as your injury prevents you from earning your full wages and you’re actively participating in your recovery.

Think of LOE benefits as a financial bridge. It’s designed to keep you stable until you can safely return to work. In cases of severe, permanent disability, these benefits can even continue until you turn 65.

Health Care and Medical Benefits

Your recovery is paramount. The WSIB provides comprehensive health care coverage so you can get the treatment you need without having to pay out of pocket. This benefit is a cornerstone of the system, removing the financial stress that can so often get in the way of proper healing.

This coverage is broad and is meant to cover all reasonable and necessary treatments, including:

- Doctor and Specialist Visits: Any appointments you need to diagnose and treat your workplace injury.

- Physiotherapy and Rehabilitation: Crucial therapies like physio, chiropractic care, and occupational therapy to help you get back on your feet.

- Prescription Medications: The full cost of any drugs prescribed to manage your condition.

- Medical Devices and Equipment: Things like crutches, braces, or specialized tools needed for your recovery are covered.

- Travel Costs: The WSIB can also reimburse you for reasonable travel expenses to get to and from your medical appointments.

To give you a clearer picture, here’s a quick summary of the main benefit types.

A Quick Look at Key WSIB Benefit Categories

Getting Back to Work Safely and Sustainably

Getting back to work is a huge step in your recovery, but it has to be done right. This isn’t about rushing you back to your old duties before you’re ready. It’s about a return that’s safe, medically sound, and won’t put you at risk of re-injury. That’s precisely why the Workplace Safety and Insurance Board’s (WSIB) return-to-work (RTW) programs are so important.

These programs are one of the core benefits of workers compensation, shifting the focus from just providing a cheque to actively helping you get back on your feet. It’s a team effort—you, your employer, and your WSIB case manager all work together. Your voice and your doctor’s input are central to building a plan that actually works for you.

You can think of your RTW plan like a personalized program from a physiotherapist. It’s a structured, goal-oriented process built around your specific physical or psychological needs, ensuring you don’t push yourself too hard and end up back at square one.

The Team Approach to Your Return

A successful return to work is never a solo mission. In Ontario, the law emphasizes cooperation between you and your employer. This team-based approach keeps everyone on the same page, all aiming for the same goal: getting you back to meaningful work safely.

Here’s how each person fits into the puzzle:

- You (The Worker): Your role is to stay in touch with your employer and the WSIB, go to your medical appointments, and be an active voice in creating and following your RTW plan.

- Your Employer: Legally, your employer must try to modify your job or workplace to accommodate your needs, unless doing so would cause them undue hardship.

- The WSIB: The WSIB acts as the facilitator. They bring in specialists and provide resources to help design and monitor the RTW plan, making sure it lines up perfectly with your medical restrictions.

This collaborative structure helps avoid confusion and ensures any plan is based on clear, current medical advice about what you can and can’t do safely.

The ultimate goal of an RTW plan is an Early and Safe Return to Work. This means finding suitable work that fits your functional abilities, respects your recovery, and helps you rejoin the workforce as soon as it’s medically appropriate.

Practical Tools for a Safe Return

The WSIB has several practical tools at its disposal to build a custom RTW plan just for you. These aren’t just about getting you back on the clock; they’re about making sure your return is sustainable and doesn’t jeopardize your health.

Modified Work Plans

From: A Guide to Benefits from Workers’ Compensation in Ontario

Your Guide to Navigating WSIB Benefits in Ontario

Think about it: your paycheque suddenly disappears, but your rent, car payments, and grocery bills don’t. A workplace injury can instantly send your life into a tailspin, creating a perfect storm of financial and emotional stress. This is exactly where Ontario’s workers’ compensation system is meant to step in and restore a sense of stability.

Overseen by the Workplace Safety and Insurance Board (WSIB), the program is a type of ‘no-fault’ insurance. What does that mean for you? It means you don’t have to get bogged down in proving your employer was somehow at fault to get help. You simply need to demonstrate that your injury or illness is a direct result of your job duties. The entire system is funded by employers, creating a province-wide safety net for workers.

The Core Purpose of Workers’ Compensation

At its heart, the system’s mission is to shield you from the harsh fallout of a job-related injury. It’s not about pointing fingers or assigning blame; it’s about providing immediate, practical support. While prevention is always the best medicine—and understanding Canadian workplace safety standards is key—accidents still happen.

When they do, workers’ compensation benefits in Ontario are built to address the critical areas of your life that get turned upside down:

- Income Stability: It replaces a large portion of your lost earnings so you can pay your bills and focus on getting better.

- Medical Recovery: The system covers the costs of essential treatments, whether it’s physiotherapy, medication, or specialized medical devices.

- Return-to-Work Support: It provides a structured path to help you get back to your job safely, or if that’s not possible, to find new work.

- Long-Term Assistance: For injuries that result in a permanent impairment, it offers benefits that recognize the lasting impact on your life.

This system acts as a crucial buffer, ensuring that one unfortunate event at work doesn’t lead to a long-term financial crisis for you and your family. It acknowledges the contributions of workers by providing a structured process for recovery and support.

This guide will demystify the WSIB process and break down exactly what kind of support you can expect. From the main benefit types to the claims process, our goal is to give you the clear, straightforward knowledge you need. For a deeper dive, you can learn more about how WSIB insurance works in Ontario in our dedicated article.

The Five Pillars of WSIB Support Explained

When you get hurt on the job, the term “benefits” can feel vague and overwhelming. In Ontario, the WSIB system is actually built on five core types of support, each one created to tackle a specific challenge you’ll face during recovery.

Think of them as the five essential pillars holding up your financial and physical well-being after a workplace accident. Getting to know these pillars takes the mystery out of the process, showing you what you’re entitled to and why. Let’s break each one down so you have a clear picture of how the benefits workers’ compensation provides can help you get back on your feet.

1. Loss of Earnings (LOE) Benefits

The first thing most people worry about after an injury is money. How are you going to pay the bills or buy groceries when you can’t work? Loss of Earnings (LOE) benefits are the financial bridge designed to carry you from the day you get hurt until you can safely return to your job.

This isn’t a token amount; it’s a significant wage replacement. LOE benefits cover 85% of your net average earnings—that’s your take-home pay after taxes and other deductions. This is calculated based on what you were making before your injury, so the support you get is directly tied to what you’ve actually lost.

This pillar is arguably the most critical for your immediate stability. It gives you the breathing room to focus on healing without the constant stress of falling behind financially, letting you follow your doctor’s orders instead of rushing back to work too soon.

2. Health Care Benefits

Beyond your lost paycheque, medical bills can pile up incredibly fast. The second pillar, Health Care Benefits, acts as your dedicated recovery fund, making sure you get the care you need without having to pay out of your own pocket.

This support is surprisingly comprehensive. The WSIB will pay for any approved treatments and services that are necessary for your recovery from the work-related injury.

Commonly covered expenses include:

- Medical Treatments: Visits to your family doctor, specialists, and other healthcare providers.

- Prescription Medications: Any drugs prescribed to manage pain, prevent infection, or help you heal.

- Rehabilitation Therapies: This includes physiotherapy, chiropractic care, and occupational therapy to rebuild your strength and function.

- Medical Devices: Things like braces, crutches, or other specialized equipment you need for mobility and recovery.

This pillar is all about removing the financial barriers to getting better. It ensures your recovery plan is dictated by your medical needs, not by what you can afford.

3. Vocational Rehabilitation

From: Navigating Ontario Work Comp Benefits: Your Complete Guide

The Four Pillars of WSIB Support You Can Claim

When you get hurt on the job, figuring out what help you’re entitled to can feel overwhelming. The best way to get your head around it is to think of WSIB benefits as a structure built on four distinct pillars. Each one is designed to support a specific part of your recovery, creating a safety net whether you’re a construction worker in Mississauga or a tech employee in Waterloo.

Knowing what these pillars are helps you see the whole picture. It clarifies which benefits fit your specific situation so you don’t miss out on crucial support that could make all the difference to your recovery and financial well-being.

Pillar 1: Loss of Earnings Benefits

Let’s be honest—the first thing most people worry about is how to pay the bills when they can’t work. That’s exactly what Loss of Earnings (LOE) benefits are for. This first pillar is your financial lifeline, designed to replace a good chunk of the income you’ve lost.

LOE benefits are calculated to be 85% of your net average earnings from before your injury. “Net” simply means your take-home pay after taxes and the usual deductions have been taken off. And it’s not just for full-time, permanent staff; this support is there for part-time, seasonal, and contract workers across Ontario.

This financial bridge is absolutely critical. It gives you the breathing room to cover your mortgage, groceries, and car payments, taking a huge weight off your shoulders. When you aren’t stressed about money, you can put all your energy into getting better. For a deeper dive into how these payments are managed, you can learn more about WSIB insurance in Ontario and the details of the coverage.

Pillar 2: Health Care Benefits

The second pillar is all about your physical and mental healing. WSIB’s Health Care Benefits cover a huge range of medical services and supplies you might need because of your workplace injury. This support is meant to be comprehensive, making sure you get the care you need without having to pay for it yourself.

These benefits aren’t just for doctor’s appointments. They’re set up to support every angle of your recovery journey.

- Medical Treatments: This covers everything from seeing specialists and having surgery to any emergency care you needed.

- Rehabilitation Services: Physiotherapy, chiropractic treatments, and occupational therapy are all included to help you get your strength and mobility back.

- Prescription Medications: Any drugs your doctor prescribes to treat the work-related injury are covered.

- Medical Devices: This can be anything from crutches and braces to more specialized equipment needed to help you function.

How to Navigate the WSIB Claim Process

Filing a WSIB claim can feel overwhelming, like you’ve been handed a complex puzzle without the instructions. But it doesn’t have to be. Let’s break down this bureaucratic process into a clear, step-by-step roadmap for Ontario workers. Knowing what to do—and when—is the key to getting the benefits you’re entitled to.

The moment you get hurt, the clock starts ticking. Your first two moves are non-negotiable: report the injury to your employer right away, and get medical attention. Don’t delay, even if the injury seems minor at first.

These initial steps are the foundation of your entire claim. Reporting the incident to your supervisor officially documents that it happened at work. A visit to the doctor provides the crucial medical evidence that connects your injury to that workplace event.

The Three Key Forms That Build Your Case

After you’ve reported the injury and seen a doctor, the real paperwork begins. The WSIB process hinges on three key documents from three different people: you, your employer, and your doctor. Think of them as the three legs of a stool—if one is missing or shaky, the whole thing can fall over.

For your claim to even be considered, these forms must be submitted:

- Your Report (Form 6): This is the Worker’s Report of Injury/Disease, and it’s your chance to tell your side of the story. It’s up to you to fill this out and send it to the WSIB. Be as detailed and accurate as you possibly can about how the injury happened and what your symptoms are.

- Your Employer’s Report (Form 7): Your employer is legally required to complete and submit a Form 7 to the WSIB within three business days of learning about your injury, but only if it causes you to lose time from work or requires more than basic first aid.

- Your Doctor’s Report (Form 8): This is the Health Professional’s Report. The doctor or health care professional who first treats you fills this out. It gives the WSIB the initial medical diagnosis and a professional opinion on your ability to work.

It is your responsibility to make sure your Form 6 gets submitted. Never assume your employer will do it for you. This is one of the most important things you can do to protect your right to benefits.

Understanding the Critical Six-Month Deadline

In Ontario, you are up against a strict deadline. You must file your Form 6 with the WSIB within six months of the date you were injured. If you’re dealing with an occupational disease that developed over time, this six-month window starts from the day you’re diagnosed and learn it’s connected to your job.

From: Workers’ Compensation Benefits: Ontario Guide to Coverage and Claims

Common Reasons WSIB Claims Are Denied and How to Appeal

Getting that denial letter from the WSIB can feel like a punch to the gut. It’s frustrating, disheartening, and can leave you wondering how you’ll manage. But it’s critical to know this: a denial is not the final word. In fact, it’s often just the starting point of a longer conversation, and you have a clear, legal path to challenge the decision.

The first move is to figure out why your claim was rejected. Denials don’t just happen randomly; they’re almost always tied to specific gaps or questions the WSIB had about your application. By zeroing in on that exact problem, you can start building a much stronger case for an appeal.

Understanding Why Your Claim Was Denied

While every situation is different, most WSIB denials boil down to a handful of common issues. Pinpointing which one applies to you is the key to building a winning appeal strategy. The WSIB adjudicator needs clear and convincing evidence, and if they feel a piece of the puzzle is missing, they’ll often play it safe and deny the claim.

Here are some of the most frequent reasons your workers’ comp benefits might get turned down:

- Missed Deadlines: The WSIB runs on a strict clock. You have six months from the date of your injury to file your Form 6. Missing this deadline is one of the quickest ways to get an automatic rejection.

- Weak Medical Evidence: Your claim is only as strong as the medical paperwork backing it up. If your doctor’s reports are vague, don’t clearly connect your injury to what happened at work, or fail to describe your physical limitations, the WSIB may decide there isn’t enough proof.

- Disputes Over “Work-Relatedness”: Sometimes, your employer might argue that the injury didn’t actually happen at work or because of your job duties. This is a common hurdle for gradual-onset issues like repetitive strain injuries or for incidents that nobody else witnessed.

- Pre-existing Conditions: The WSIB or your employer might suggest that your pain and symptoms are caused by an old injury or a condition you had before the workplace incident, not the new event.

A denial isn’t a judgment on whether your injury is real; it’s simply a decision based on the information they had at the time. The appeals process is your chance to provide new, better, or clearer information to get that decision overturned.

The WSIB Appeals Process Step-by-Step

If you disagree with the WSIB’s decision, you don’t just call up the original case manager to argue. Instead, you enter a formal, multi-level appeals system designed to give your claim a fresh set of eyes.

From: Workers Compensation Guide: Your Rights & Employee Benefits in Ontario

How WSIB Protects Ontario Workers

Think of Ontario’s Workplace Safety and Insurance Board (WSIB) as a mandatory insurance plan that covers almost every workplace in the province. It’s not an optional extra; it’s a legal requirement put in place to protect people who get hurt or become ill because of their job.

The most important thing to understand about the WSIB system is that it’s “no-fault.”

This “no-fault” principle is the bedrock of the entire system. It means you don’t have to prove your employer did anything wrong to cause your injury. If you were hurt while doing your job, you’re entitled to benefits. It’s that simple.

This is a game-changer for injured workers. It means you can focus on getting better instead of gearing up for a long, expensive court battle to prove who was at fault.

What Kinds of Injuries Are Covered?

WSIB coverage is surprisingly broad and isn’t just for dramatic, one-time accidents. It’s designed to cover the many ways a job can affect a person’s health over time.

Generally, the injuries and illnesses covered fall into a few key areas:

- Traumatic Accidents: These are the sudden events we often picture—a slip and fall, an injury from machinery, or hurting your back while lifting something heavy.

- Repetitive Strain Injuries: These injuries don’t happen overnight. They build up from doing the same motions again and again, like carpal tunnel syndrome from typing or tendonitis from working on an assembly line.

- Occupational Diseases: Sometimes, the workplace itself can make you sick. This category covers illnesses from being exposed to harmful substances or conditions, like lung disease from breathing in dust or hearing loss from years of loud noise.

- Mental Stress: In specific circumstances, WSIB will also cover mental health conditions that are a direct result of a traumatic workplace event or ongoing workplace harassment.

This comprehensive approach makes sure you’re protected whether your injury happened in a single moment or developed slowly over years of hard work.

The Core Benefits WSIB Provides

When WSIB approves your claim, you get access to a bundle of benefits designed to keep you financially stable and help you recover. It’s not just a single cheque; it’s a structured support system.

The main benefits you can expect are:

Understanding Your Group Employee Benefits Package

Think of it this way: WSIB is a specialized safety net just for work-related injuries. Your group employee benefits package, on the other hand, is the much broader support system for your overall health and well-being, both on and off the clock. It’s essentially a private health plan your employer has arranged for you and your colleagues.

This package is designed to kick in for all the life events and health challenges that have nothing to do with your job. For instance, if you slip on an icy sidewalk while walking your dog on a Sunday and break your ankle, that’s where your employee benefits come into play. If you’re diagnosed with an illness that forces you to be off work for months, your disability benefits are what you’ll rely on for income. These are private insurance policies, not a government program like WSIB.

The Key Components of Your Benefits Plan

Most group benefits packages in Ontario share a similar structure, even if the specific coverage amounts differ between employers. They are typically built around providing income replacement if you can’t work and helping cover day-to-day medical expenses.

It’s crucial to remember that these plans are governed by a detailed insurance contract, not a piece of provincial legislation like the Workplace Safety and Insurance Act. Your rights, the rules, and the claim procedures are all laid out in the policy documents from the insurance company.

Here’s what you’ll usually find inside:

- Short-Term Disability (STD): This is your first line of defence. It replaces a portion of your income for a limited time—often up to six months—if a non-work-related illness or injury keeps you from your job.

- Long-Term Disability (LTD): When STD runs out, LTD is designed to take over. If you’re still unable to work, this benefit can provide a percentage of your income for a much longer period, sometimes all the way to age 65.

- Extended Health Coverage: This helps pay for many medical expenses that the Ontario Health Insurance Plan (OHIP) doesn’t cover. Think prescription drugs, physiotherapy, vision care, or specialized medical equipment.

- Dental Coverage: This part of the plan helps with the costs of everything from routine cleanings and fillings to more significant procedures like crowns or orthodontics.

How Disability Benefits Actually Work

Navigating a disability claim, especially for Long-Term Disability, is a completely different ball game than filing with WSIB. The first thing you need to understand is the “elimination period,” which is just an industry term for a waiting period. This is a specific amount of time you must be continuously disabled and off work before your LTD benefits can even start.